This story is part of CNBC Make It’s Millennial Money series, which profiles people around the world and details how they earn, spend and save their money.

Todd Baldwin has always wanted to make a lot of money. “I was raised by a single mom, and I watched her struggle working four jobs to try to feed three kids,” the 27-year-old self-made millionaire tells CNBC Make It. “She was worried all the time about money. I saw it. I could feel it.”

Baldwin didn’t want to experience the same financial stress when he grew up, so at 12, he started working. His first job was shoveling manure for $3 an hour: “I came home one day, and I counted up six dollars worth of quarters. At the time, it was more money than I had ever seen. Since that moment I was like, I’ve got to make millions of dollars.”

He achieved that goal at 25 when his net worth crossed $1 million, thanks to smart real estate investing with his wife, Angela. Today, he brings in $615,000 annually thanks to a mix of income from rental properties, his day job working in commercial insurance sales and the extra cash he makes as a secret shopper. After real estate expenses, his take-home pay is closer to $305,000. Angela brings in another six figures from her 9-to-5, a paycheck they almost entirely save.

The Baldwins live “very comfortably,” he says. But he still has lofty money goals: By 35, he wants his net worth to hit $10 million.

That’s one of the reasons he and Angela live well below their means. “Although our net worth is seven figures, we don’t do a lot of the typical things that most people envision millionaires doing,” says Baldwin, who wears a $12 rubber wedding band. “We are super frugal.”

They have roommates, drive a 2009 Ford Focus and their monthly food bill rarely exceeds $25, thanks to all the free meals they get as “secret shoppers.”

Because Baldwin keeps his expenses so low, he’s able to save more than 80% of his take-home pay, he tells CNBC Make It: “Out of the $615,000 I bring in, I invest almost all of that back into more real estate, so I don’t actually see a lot of it.”

Here’s a closer look at how he earns, spends and saves his money.

What he earns

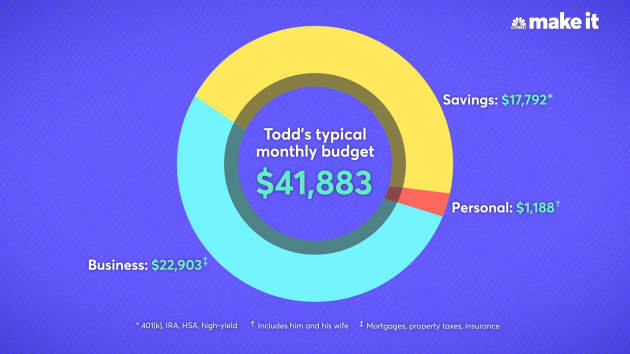

Here’s a breakdown of Baldwin’s typical monthly income as of December 2019.

His day job

After dropping out of Western Washington University in 2014, Baldwin landed a sales job in the commercial insurance industry. His starting salary was $50,000, but after several high-performing months, he doubled it to $100,000 in less than a year.

Today, his salary from his day job is $150,000.

Real estate income

The bulk of Baldwin’s revenue, though, comes from real estate. He and his wife own six rental properties worth over $4 million and bring in about $460,000 per year in rent, or $38,300 per month. After expenses, including mortgage payments, taxes, insurance and utilities, they keep about $150,000 of that per year, or $12,500 a month.

Baldwin and his wife bought their first property when they were 23. They were looking to rent but the prices in Seattle were too high. Instead, they decided to buy their own place and rent out the extra bedrooms to offset the cost. Their first place cost $506,000 when they bought it in December 2015. They had enough in savings to put $19,000 down, about 3.5%.

Nine months later, they bought their second property, “and it just kept snowballing,” says Baldwin. “Now, we have a total of six houses.” Today, their real estate portfolio is valued at $4.4 million. They owe about $3.1 million in mortgages, and those costs are being covered by their many tenants.

Rather than renting out each house to a single tenant, they rent out each bedroom.

This takes a lot of upfront work, Baldwin says, from showing the rooms to potential tenants and making sure roommate personalities match up to ensuring all the rent gets paid on time each month: “When I first started out, I was working 16-hour days. It’s a lot less than that now, but we had to sacrifice a lot to get to where we are today.”

His long-term goal is to own 6,000 apartment units by the time he’s 60. “At an average of $1,500 apiece, that would be $9 million a month,” he calculates.

Secret shopping

Baldwin earns another $5,000 a year from secret shopping.

“There are a lot of businesses out there that want to know how their employees are doing and how the market is responding to their products,” Baldwin explains. “So those companies will hire mystery shopping firms to find independent contractors like me to go pose at their establishment as a regular customer, buy the product or service and then report on it.”

He started mystery shopping in college, when he was first dating his wife. “I wanted to take her out, but I didn’t have any money,” he recalls. “So I started researching ways to get free food and free entertainment, and I found this thing called secret shopping.”

At first, “I thought it was a total scam,” he admits. After all, besides getting reimbursed for dining out, going grocery shopping, seeing a movie, even visiting hotels and casinos, you get paid for your time. He tried it out anyways and got a check in the mail two weeks later. Ever since, he and Angela have been getting paid to go on dates.

“To date, I’ve made just over $30,000 from secret shopping,” he says. “And the best part is, it’s all things that my wife and I would normally do anyway. We’re going to go out to dinner, we’re going to go out to the movies. Now, we’re just getting paid to do it.”

How he budgets

Of the $615,000 Baldwin brings in, a chunk of that goes toward business expenses, including mortgage payments, taxes and insurance. Another big slice goes directly to savings — and a sliver goes toward personal expenses for him and his wife.

Here’s a breakdown of his and his Angela’s shared personal expenses, which they pay for with his income. As for Angela’s six-figure income, they save most of that in a bank account. It acts as their “travel fund” if they ever want to plan a trip.

The numbers reflect their spending activity as of December 2019.

Mortgage: $4,700

Baldwin and his wife live in a duplex in Burien, Washington, about a 15-minute drive from downtown Seattle, that they bought for $900,000 in August 2019.

Their mortgage payment, including taxes and insurance, is $4,700 per month, but the costs are entirely covered by income they earn from renting out rooms in the house. They make $3,000 per month in rent from the second half of the duplex and another $1,500 per month from the garage, which they converted into a studio apartment.

Plus, they rent out two of the bedrooms in their half of the duplex, one for $1,200 and the other for $800. That’s $6,500 in rental income, which means they net roughly $1,800 a month.

Gym memberships: $130

Baldwin, who boxed in high school, pays $100 to train at a mixed martial arts (MMA) gym. Plus, he’s a member of LA Fitness, which costs $30 a month.

“It’s well worth it because your health is your wealth,” he says. “It doesn’t make sense to be the richest man in the graveyard.”

Gas: $80

The couple shares one car, a 2009 Ford Focus, which they paid off four years ago. Baldwin spends about $80 a month filling up the tank, and then gets oil changes and other basic maintenance procedures reimbursed through secret shopping programs. He even gets free gas sometimes.

He plans to upgrade his car in a few years. “I’m not a showy or flashy guy, but I do want the Tesla Roadster,” says Baldwin. “I want it because it’s the fastest car in the world. I’ve got a lot of places to be and zero time to waste.”

While he says he could afford the $200,000 car today, he made a promise to himself that he wouldn’t buy a luxury car in his 20s. But the day he turns 30, he says, he’ll make the splurge.

Food: $25

Thanks to secret shopping, the couple spend just about $25 a month on food: “90 to 95% of our restaurant budget is covered by mystery shopping,” he says, adding: “Every once in a while, we’ll want to go somewhere a little bit more exotic that doesn’t have a mystery shopping program.”

He even gets paid to stock his fridge and pantry, once earning ”$350 to get $70 worth of groceries from Trader Joe’s,” he says.

Anyone can become a secret shopper, but you have to put in the time before landing the best-value gigs. One of Baldwin’s first experiences was at fast-food chain Five Guys, he recalls: “I got a free meal, plus about $4 worth of profit, so it wasn’t that big. That’s where you’re going to start, with places like Five Guys or Panda Express. But eventually, as you get a good reputation and your ranking increases, you can get really high-end restaurants.”

Credit card annual fees: $6

Baldwin has 13 credit cards. “I don’t carry balances on any of them,” he says. “I use a strategy called credit card churning, which is when you open up a new credit card, take advantage of that new account bonus, pay it off completely and then rinse-and-repeat with the next card.”

He doesn’t spend money he wouldn’t normally spend just to cash in on the rewards, he notes: “For example, when we were converting our garage apartment into an Airbnb, I knew that there were going to be expenses with that, so I opened up a new credit card where if you spend a $1,000 in the first three months, you get $200 cash back.

“I’m not telling anyone to go out of their way to spend $1,000 to make $200 — that’s an $800 loss — but for us, we would have spent that $1,000 anyway, so we might as well take advantage of the $200 we can get in cash back.”

Among his 13 cards, one has an annual fee, a travel rewards card, which he pays about $6 a month for.

Other: $947

- Insurance: $550 (car, health, life)

- Utilities and Wi-Fi: $300

- Phone: $67

- Subscriptions: $30 (Netflix, Hulu)

How he saves

Baldwin sets aside about 80% of his take-home pay in various accounts. Every month, he puts $8,000 in a high-yield savings account for future real estate purchases; another $5,000 goes into a separate high-yield savings account for retirement; plus, he maxes out two IRAs and two 401(k)s — his and his wife’s — and a health savings account (HSA).

In 2019, he put $6,000 in both his and his wife’s IRAs, $19,500 in both of their 401(k) plans and $7,100 in his HSA. Any extra money they have left at the end of each month goes toward savings or a vacation.

It helps that he brings in a lot of revenue from his real estate holdings, but in order to save so much, “we’ve put a lot of fun on hold,” says Baldwin. “In our early 20s, we were sacrificing a lot of time, a lot of vacations and all the fun things that most people do in their 20s. Now that we’re at a point where we can kind of take a step back and enjoy it. We definitely want to travel the world, I want to buy my Tesla Roadster when I’m 30 and we want to have a lot more fun.”

The couple, whose net worth is closer to $1.5 million today, “could probably retire now,” says Baldwin, but an early retirement doesn’t interest him just yet. “Our goals are so much loftier than that — I want my 6,000 apartments by the age of 60.”

Plus, “I don’t know if I’m ever the type of person to truly retire in the traditional sense,” he adds.

He’d be fine taking a step back from work though when he and his wife start a family, which they want to do in the next couple of years.

“It’s nice knowing that we can pay for their college, and we can go on family vacations, but the biggest thing is being able to be a present father,” says Baldwin. “There’s no need for me to go spend eight hours a day in an office if I don’t want to, because we built systems, we built businesses and we have enough passive income so if I want to be home with the kids and be there for every ballet recital or little league game, I can. That was a huge motivation. That’s why I sacrificed so much of my time in my early 20s.”

What the expert says

CNBC Make It spoke to Ashley M. Fox, founder of Empify and a personal finance coach with experience managing the assets of high net worth individuals, to get her thoughts on what Baldwin is doing right with his money and where he could improve.

He can create more specific savings goals

Baldwin is smart to use a high-yield savings account, where your money can grow much more than in a standard savings account that offers negligent returns, says Fox. To take his finances to the next level, though, he should open multiple accounts for specific savings goals.

For example, since he and his wife want to start a family one day, they should start an account specifically for the costs associated with having a kid.

When it comes to figuring out how much to save for a your first kid, work backwards, says Fox: “Start to picture and create that life with a child. Start planning the nursery. Think about what kind of house you want to live in. Start to paint the picture of what you want, without money being an issue, and then reverse engineer it to figure out how much it’s going to cost to give your child this life.”

Next, begin setting aside a certain amount of money each month, or every time your paycheck lands, in order to reach that amount by the time you need it.

You can use a similar strategy for other goals. If you’re saving up for a car or home, think about what your life will look like with it and what new expenses will come into play. For a car, you’ll need to factor in gas and maintenance. For a home, think about the cost of insurance, taxes and renovations. Once you have a dollar amount in mind, start saving.

Ideally, you’ll have a separate account for every goal, adds Fox.

He should consider opening a brokerage account

Baldwin is doing a great job of maxing out his retirement accounts, says Fox. And while it’s OK to keep some of his money across high-yield savings accounts, it shouldn’t be the only place he stashes his cash.

Fox recommends he open a brokerage account so he can invest in the stock market, where the returns will likely be much greater than those from a high-interest savings account. “If he’s happy with where his money is invested in his IRA and his 401(k), he can duplicate that same strategy — he can take those same investments and put them in a brokerage account,” she explains. “For example, if he has Vanguard’s S&P 500 fund in his IRA, he can take that same investment, and he can also invest it in his brokerage account.”

Unlike an IRA or 401(k), there’s no cap on how much money you can put in a brokerage account. Plus, the money is more accessible, notes Fox: “You have access to your brokerage account tomorrow if you want.” The money in his retirement accounts, on the other hand, is tied up — he can’t touch it before age 59 ½ without owing a penalty.

Fox also cautions him about having the majority of his money invested in properties. “If times get rough,” says Fox, “you can’t sell a property tomorrow, but you can sell a stock today.”

He’s ambitious, but he can think bigger

Baldwin is a “dreamer,” says Fox, and that’s a good thing. “He’s very ambitious. He doesn’t want to stay where he is.”

That said, he shouldn’t be focused so much on the age at which he wants to accomplish his financial goals. Rather than setting the goal of having 6,000 apartment units by age 60, for example, he should start with a dollar amount, Fox says: “Ask: What do I want to have coming in on a consistent basis for me to feel comfortable and to accommodate my lifestyle?”

Once he answers that question, he can work backwards to figure out what it will take to generate that amount of income — and he might be able to get there a lot sooner than age 60. “I think he’s selling himself short by making his goal by 60,” she adds. “What if you can get to that point in life in the next 10 years?”

Along similar lines, Baldwin shouldn’t feel the need to wait to buy his Tesla if he can afford it today. “Why wait until 30, when you’ve been excellent up until this point?” says Fox. “Why don’t you feel like you deserve the car right now? If you can afford it now, go for it. If not, start saving for it.”

Fox believes in treating yourself when you’ve earned it: “We want to work so hard, but we don’t celebrate the small wins.” There’s no need to delay gratification if you are worthy of having want to you right now, she says.

So if you are looking for a best home that fits your style, please don't hesitate to ask ME questions and I can definitely help you out with your inquiries.

Source: CNBC